NEW RESTRICTIONS ON CRYPTO-ASSET MARKETING

Martina Hoffard, Head of Marketing, Spectrum Markets, explains Spain’s move to control the promotion of crypto-assets

Why have a conversation about the Pilot Regime? Even people who are sceptical about the benefits of crypto-assets such as bitcoin agree that the underlying technology has many potential benefits.

It used to be said that one of these benefits was disintermediation. In other words, would there be a need for CSDs, custodians, market operators or CCPs in the future marketplace if DLT could be relied upon instead? In fact, various so-called proof of concept (PoC) and minimum viable product (MVP) projects produced by new and established market participants worldwide over the past three to four years have shown that complete disintermediation does not work within existing legal and regulatory frameworks. As a matter of fact, there are good reasons why the capital markets have regulated market participants performing these roles, all of which come down to instilling trust; risk management, liability allocation, customer services, AML monitoring, to name a few.

But what if this fairly new technology was combined with appropriately regulated market participants resulting in some very real tangible benefits to the capital markets such as reducing costs and risks and increasing automation and resilience? These benefits have long been known to market participants. However, legal and regulatory uncertainty has significantly slowed down any widescale development and adoption of digital market infrastructures in this space.

This potential alone warrants a conversation about the Pilot Regime. And yet, there is another aspect which certainly adds to its appeal. Under the current EU legal and regulatory framework, transactions in securities admitted to trading or traded on a trading venue such as a regulated market, an MTF or an OTF, must be recorded in book-entry form in a CSD. This effectively means that those securities require the settlement by a CSD. Under the Pilot Regime, this requirement is softened, providing interesting opportunities for new as well as established market participants.

The Pilot Regime in one sentence

The Pilot Regime lays the foundation for the trading and settlement of certain DLT-based financial instruments without necessarily requiring the involvement of a CSD.

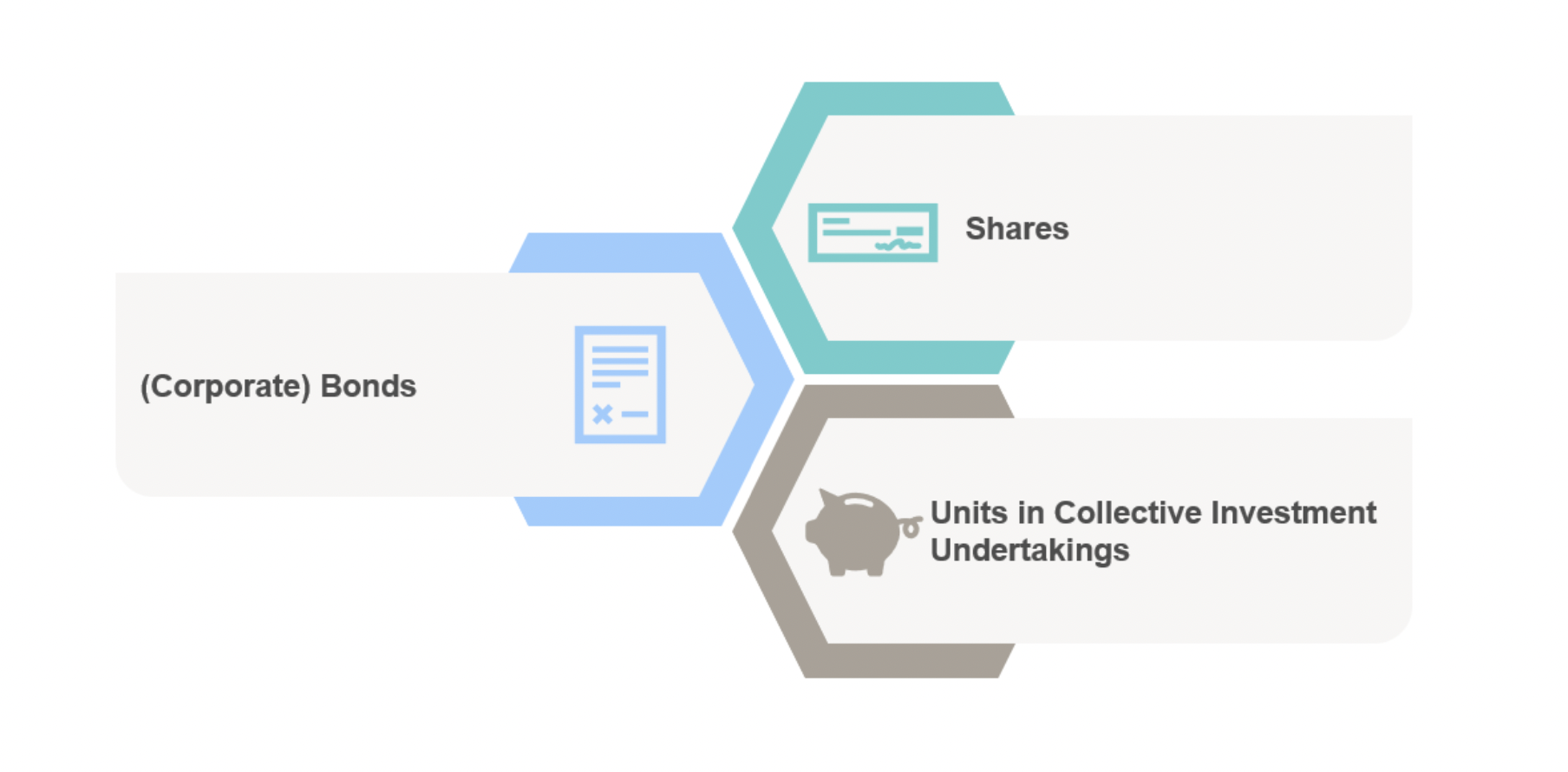

Which financial instruments are covered by the Pilot Regime?

Initially, the DLT-based market infrastructures introduced by the Pilot Regime (such as DLT MTFs, DLT Settlement Systems or DLT Trading and Settlement Systems) will generally be available to DLT financial instruments. These are financial instruments which are issued, recorded, transferred and stored using DLT. In addition, the financial instrument must fall within one of the categories set out in the chart below.

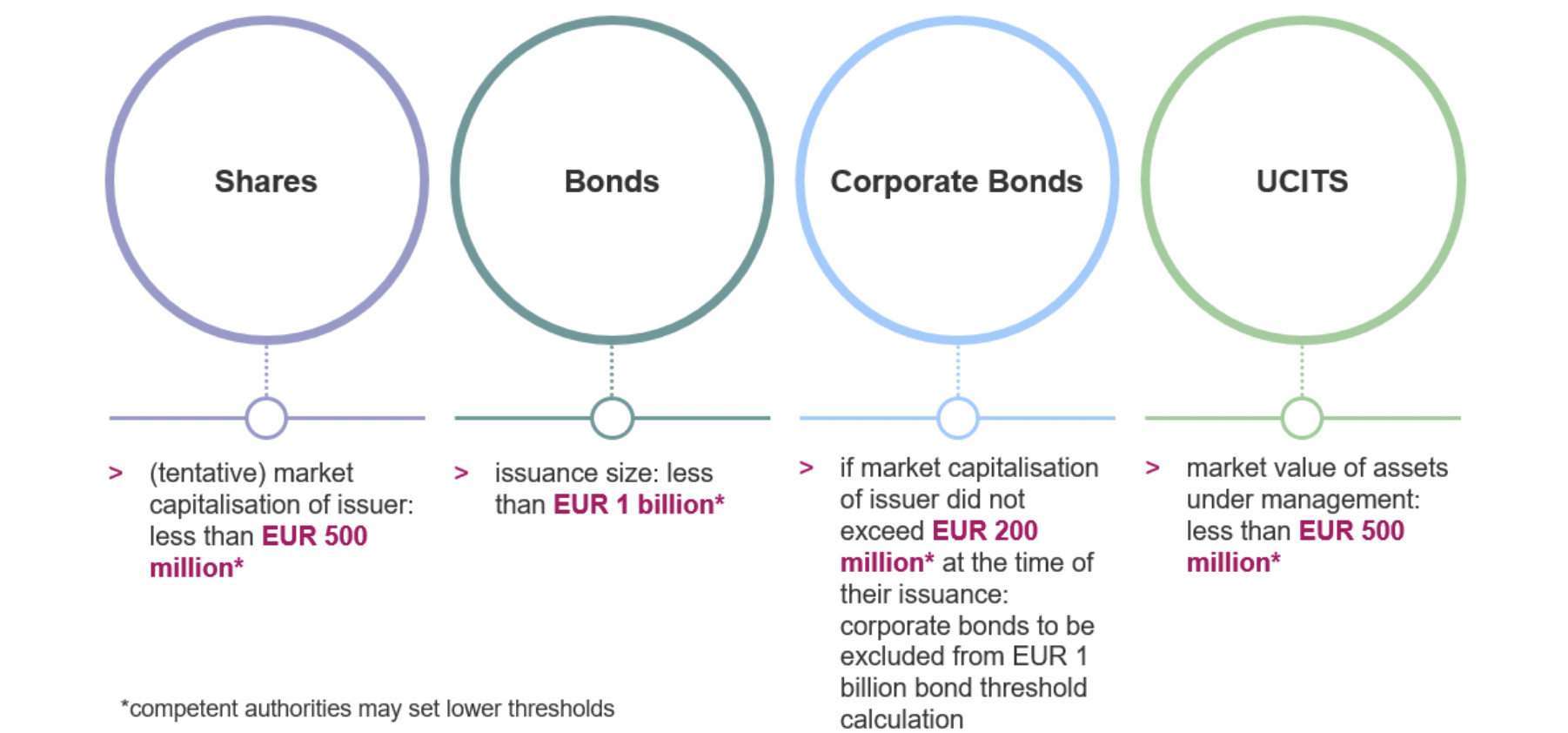

Under the Pilot Regime the DLT financial instruments are subject to certain thresholds. Depending on the category of the DLT financial instrument, different anchor points apply: For shares it is the market capitalisation of the issuer. For bonds the anchor point is the issuance size and for units in collective investment undertakings (UCITS) it is the market value of assets under management. The respective thresholds will be considered at the moment of admission to trading or the recording of the DLT financial instrument on the distributed ledger. The chart below provides an overview over the thresholds.

To avoid the creation of risk to financial stability, the total market value of the DLT financial instruments admitted to trading or recorded per DLT-based market infrastructure, i.e., each DLT MTF, DLT Settlement System or DLT Trading and Settlement System, is limited. The limit is initially set at €6bn. National competent authorities may, however, set lower limits.

What does the Pilot Regime mean for issuers?

One point to note here is that the Pilot Regime does not address how DLT financial instruments are issued and how they can be legally transferred. Those aspects are subject to and governed by national laws. For example, in Germany the process of how to issue a crypto security (Kryptowertpapier) and how to transfer it is governed by the recent German Electronic Securities Act (eWpG).

Under the current legal and regulatory framework, crypto securities issued under the eWpG can neither be traded on regulated markets, MTFs nor OTFs. In other words: The trading of crypto securities is limited to OTC market making crypto securities - unlikely to be used for refinancing purposes. However, under the Pilot Regime, crypto securities will generally become eligible for trading on DLT MTFs making them more appealing to investors.

Why become a DLT MTF?

One opportunity is to take advantage of the clarification of the regulatory framework for DLT models and to benefit from the exemptions that apply to DLT MTFs compared to traditional MTFs. For established MTF operators this could mean exploring a business model for DLT financial instruments under simplified conditions. Potential new operators could gain access to the market without having to comply with the full set of requirements applicable to traditional MTFs.

There is another aspect to be taken into account (when considering becoming a DLT MTF) and this aspect is a novum. Under the current EU legal and regulatory framework, it is not permissible to combine trading and settlement within one legal entity (irrespective of the technology being used). However, under the Pilot Regime the trading and settlement of DLT financial instruments can be combined in the role of a DLT TSS (trading and settlement system).

DLT TSS – a game changer?

The introduction of the DLT TSS is quite remarkable. A DLT TSS is a combination of a DLT MTF and a DLT settlement system, thus bringing together the benefits of DLT by combining trading and settlement (in near-real-time). A DLT TSS can be operated by investment firms and market operators under the MiFID II regime as well as by CSDs under the CSDR regime.

This “one stop shop” represents the only DLT market infrastructure under the Pilot Regime that can offer both trading and settlement of DLT financial instruments. This makes the DLT TSS clearly superior to other DLT market infrastructures. Only the DLT TSS is in a regulatory position to exploit all the advantageous functionalities and thus the full potential of DLT such as:

There are significant opportunities here for CSDs and operators of MTFs/trading venues alike.

What does the Pilot Regime mean for investors?

First of all, the Pilot Regime does not impact the performance of the relevant DLT financial instrument. The fact that a financial instrument is issued, recorded, transferred and stored using DLT does not change its legal content.

Under the Pilot Regime investors (including certain retail investors) can directly connect to a DLT market infrastructure without the need for an intermediary such as a custodian (as is the case under the current legal and regulatory framework).

Another advantage from an investor’s perspective is the tradability of DLT financial instruments and the speed at which those instruments can potentially be traded and settled. This makes them suitable objects for various types of securities lending, repo and collateral transactions.

Investors may also benefit from lower transaction costs resulting from new market players potentially entering the market.

What’s next?

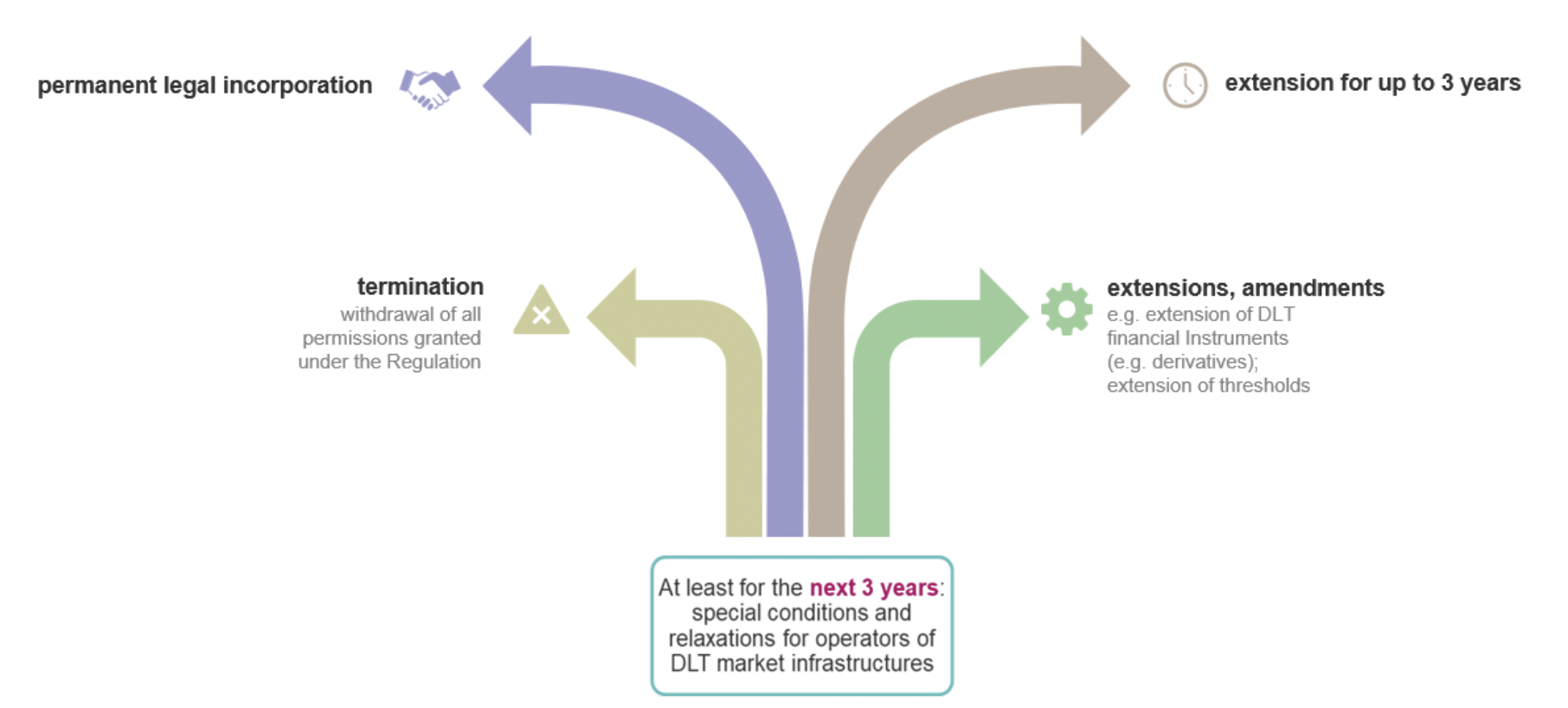

The Pilot Regime will initially apply for three years after which ESMA will prepare a report to the Commission on the overall functioning of the DLT market infrastructures. The report will include, among other things:

In summary, it can be said that the sandbox created by the Pilot Regime provides a safe and regulated playground to further explore what DLT has to offer, while at the same time introducing a number of interesting new features such as the DLT TSS. Ultimately, it will be up to market participants to put the sandbox to good use, in the process maybe making it a permanent feature of the capital markets playground. As such, at least on paper, the Pilot Regime has the potential to be the next stop on the journey, with near-real-time trading and settlement of financial instruments as the final destination.

Get in touch today to discuss how the seamless market access that our venue provides, can help to grow your retail client business.