AN ERA OF COMPETITIVE GOVERNANCE

There has been some debate about whether regulatory divergence between the financial sectors of the European Union (EU) and the United Kingdom (UK) following Brexit is ante portas.

All information contained herein is for information purpose only and addresses exclusively Members of Spectrum Markets and persons interested in becoming a Member of Spectrum Markets. Nothing herein constitutes an offer to sell or a solicitation of an offer to purchase any securitised derivatives listed on Spectrum Markets or any product described herein. Spectrum Markets does not provide financial services, such as investment advice or investment brokerage. Prospective retail investors can trade such products only with their brokers. The information herein does not constitute investment advice or an investment recommendation. Any information provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. Turbo Warrants are complex financial instruments and investors may experience a total loss.

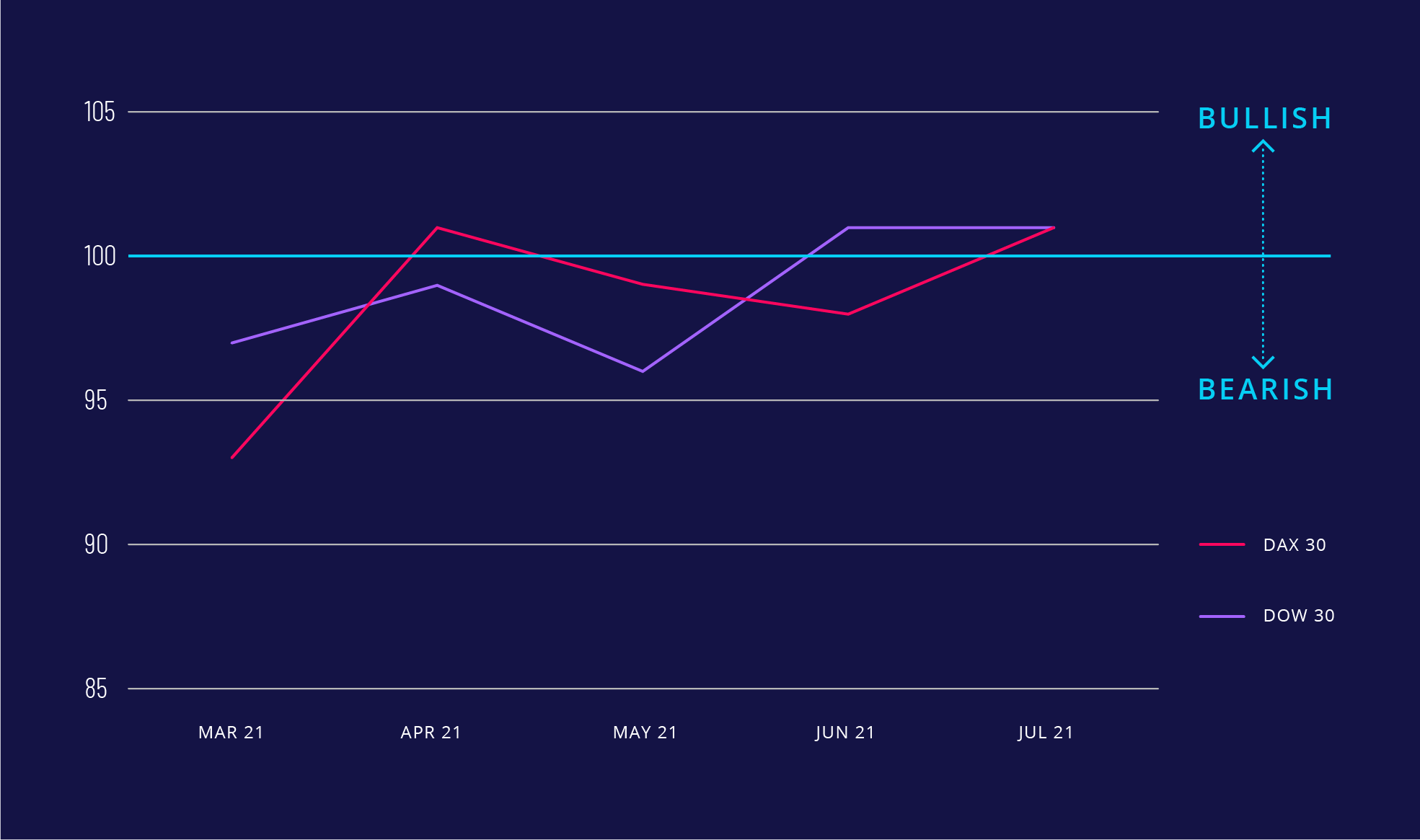

And there’s good news for equities markets: the July SERIX™ indexes for the DAX 30 and the DOW 30 are Bullish! For the DAX 30, it’s the first time in bullish territory since April 2021. And for the DOW 30, the trend came from Bearish to Bullish territory.

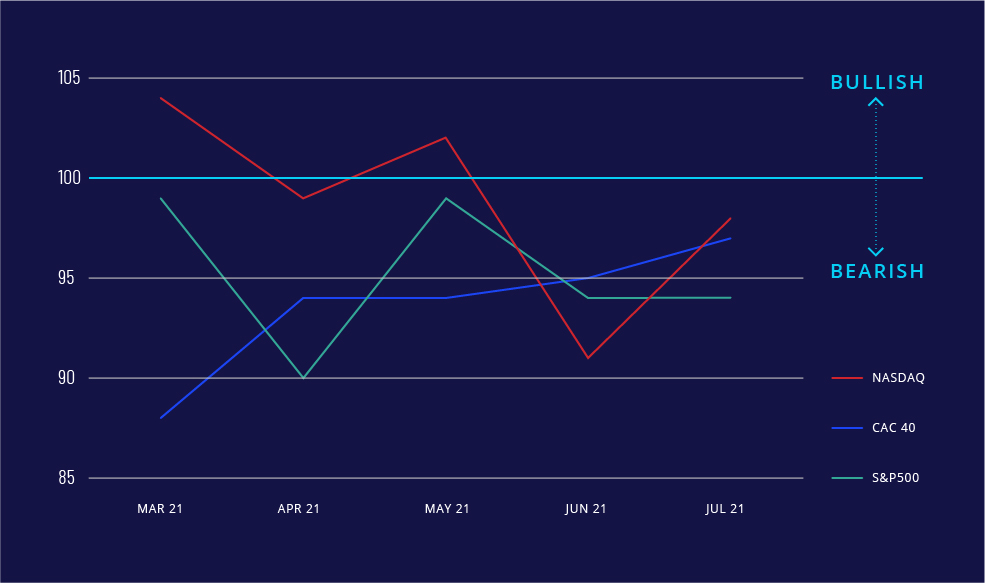

However, we have to be cautious because for the CAC 40, NASDAQ 100 and the S&P 500, it’s the opposite path; from Bullish to Bearish. In other words, investors want to remain optimistic, but are worried nevertheless.

The same can be seen in the evolution of the latest leading indicators of economic activity throughout the world, especially Markit Purchasing Manager Indexes. (‘composite’ = all sectors)

More fundamentally, and independently of Covid19, the summer period is often conducive to high stock market volatility. Even if there is no rational explanation, we must recognise that the summer period is often synonymous with bad times for the stock markets. Out of the last eleven summers from 2005 to 2015, only three were positive for the markets; 2006, 2012 and 2013.

On the other hand, since 2016, the trend has completely reversed. Over the last five summers, international stock market evolution (particularly in the United States and France) has been consistently positive.

In this context, the summer of 2021 has a very special significance because it will tip the balance, either towards the return of the ‘murderous summer’, or towards the confirmation of the summer stock market euphoria.

The summer of 2016 marked the beginning of an incredible phase of resilience in the stock markets. Since that date, they have weathered all the storms without a hitch. Brexit, political crisis in Italy, the rise in the Fed’s key rates and even the coronavirus pandemic.

Nothing has hindered the rise of stock market indices. They have certainly experienced some difficult times, particularly in the autumn of 2018 and March 2020, but have constantly climbed the slope, especially during the summer periods. This is mainly thanks to the ultra-dovish action of central banks, which have flooded the financial markets with free liquidities.

However, ‘nature’ also has its limits; trees do not rise to heaven. So, let’s not forget that the stock markets continue to revel in a bubble, to the extent that their valuation is excessive given economic reality.

A simple comparison shows this; from 1997 to 2021, global GDP in value terms (adjusted for inflation) grew by 170% at best, while over the same period, the Dow Jones exploded by 430%. That’s 2.5 times more. In the face of such extravagance, how can we continue to refuse to admit that the stock markets are stuck in a bubble that is swelling day by day? Moreover, in the summer of 2021, four major risks threaten global stock markets and could trigger a downward correction.

To conclude, as the SERIX™ data shows, the 2021 summer will be particularly hot, especially for the bond and stock markets. Of course, an alternative scenario exists: if the pandemic is definitively brought under control, financial markets could become less volatile and even positive at the end of the year. Anyway, it will be essential to remain very careful, sail on sight. Or even, for the most adventurous, make regular round trips. Happy holidays anyway, and good roller coasters to all.

Thank you very much!

Get in touch today to discuss how the seamless market access that our venue provides, can help to grow your retail client business.